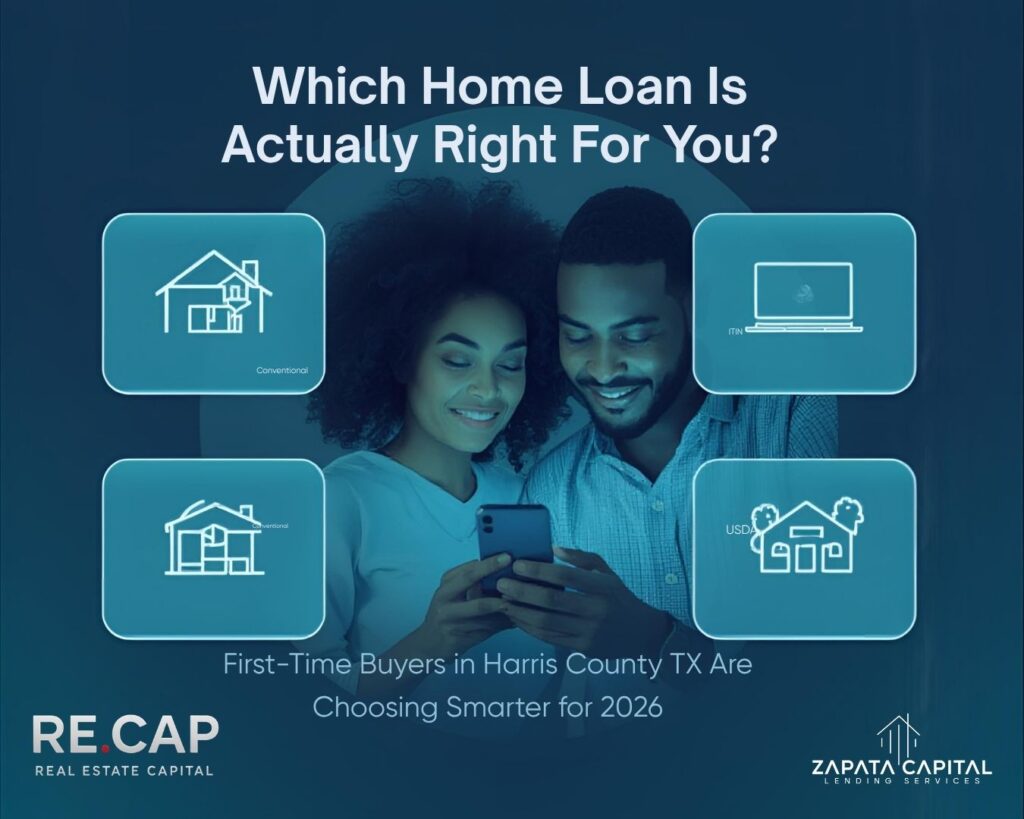

What Are Your Best Options?

If you’re searching for the best first time home buyer loans in Harris County TX, you’re not alone. With home prices shifting across Houston, Katy, Cypress, and surrounding areas, more buyers are trying to figure out which loan actually makes sense—not just which one they qualify for.

The truth is, most first-time buyers don’t fail because of income. They struggle because they choose the wrong loan strategy.

In a market as competitive and diverse as Harris County, understanding your options can save you thousands—and in some cases, make the difference between getting approved or denied.

Why Loan Choice Matters in Harris County TX

Harris County isn’t a one-size-fits-all housing market.

You’ve got:

- Entry-level homes in Houston

- Growing suburban communities like Katy and Cypress

- Outer areas where zero-down programs may still apply

Because of this, the best first time home buyer loans in Harris County TX depend heavily on:

- Your income type

- Credit score

- Debt level

- Citizenship or residency status

Let’s break down the most relevant loan options and where they actually fit.

Conventional Loans: The Best Long-Term Option for Qualified Buyers

For many buyers, conventional financing is the strongest choice—if you can qualify.

Conventional loans work best if you:

- Have stable W-2 income

- Maintain a credit score above 620 (ideally higher)

- Keep your debt-to-income ratio under control

What makes this one of the top first time home buyer loans in Harris County TX is the long-term savings:

- Low down payment options (as little as 3%)

- Competitive interest rates

- No permanent mortgage insurance

- Lower total cost over time

In areas like Houston, Katy, and Cypress, conventional loans are often used for buyers who want stronger offers and better financial positioning.

Bottom line:

If you qualify, this is usually the smartest financial move.

FHA Loans: The Most Accessible First-Time Buyer Loan

Not everyone walks in with perfect credit or large savings—and that’s where FHA loans come in.

FHA loans are one of the most common first-time homebuyer loans in Harris County, TX, because they’re more forgiving.

They allow:

- Down payments as low as 3.5%

- Lower credit score requirements

- Higher allowable debt ratios

This makes FHA ideal for:

- First-time buyers with moderate income

- Buyers recovering from credit issues

- Those who need flexibility to qualify

Across Houston, FHA loans are often the starting point for buyers entering the market for the first time.

Reality check:

You may pay more in mortgage insurance—but you get into a home sooner.

Non-QM Loans: A Solution for Self-Employed Buyers

Harris County has a large population of entrepreneurs, freelancers, and business owners. If that’s you, qualifying for a traditional loan can be frustrating.

That’s where Non-QM loans come in.

These are designed for buyers who don’t show income the “traditional” way.

Instead of tax returns, lenders may use:

- Bank statements

- 1099 income

- Business cash flow

This makes Non-QM one of the most flexible first time home buyer loans in Harris County TX for:

- Self-employed individuals

- Business owners with write-offs

- High-income earners with complex finances

The trade-off?

- Higher interest rates

- Larger down payments

But for many buyers in Houston, it’s the difference between buying now—or waiting years.

ITIN Loans: A Key Option in Harris County

Houston is one of the most diverse housing markets in the country, and many buyers don’t have a Social Security Number.

ITIN loans are specifically designed for:

- Non-U.S. citizens

- Borrowers filing taxes with an ITIN

- Buyers with verifiable income but non-traditional documentation

These loans open the door to homeownership for a large portion of the Harris County population.

They typically require:

- Higher down payments

- Alternative credit evaluation

But they remain one of the most important first time home buyer loans in Harris County TX for underserved communities.

USDA Loans: Zero Down Opportunity (If Location Qualifies)

USDA loans are often overlooked—but they can be one of the best deals available.

They offer:

- 0% down payment

- Competitive interest rates

- Reduced mortgage insurance

The only limitation is location.

While central Houston won’t qualify, some outer areas of Harris County and nearby regions do.

For buyers willing to live just outside dense urban zones, USDA can be one of the most powerful first time home buyer loans in Harris County TX.

Comparing First Time Home Buyer Loans in Harris County TX

Here’s how these options realistically stack up:

- Conventional Loans → Best for strong credit and stable income

- FHA Loans → Best for lower credit and smaller down payments

- Non-QM Loans → Best for self-employed or complex income

- ITIN Loans → Best for non-U.S. citizen buyers

USDA Loans → Best for zero down (location-based)

What’s the Best Loan for You?

The best first time home buyer loan in Harris County TX depends entirely on your situation.

Here’s a simple way to think about it:

- If your finances are clean and straightforward → go Conventional

- If you need flexibility → FHA is your entry point

- If you’re self-employed → Non-QM is likely your path

- If you don’t have an SSN → ITIN loan is your solution

If you want zero down → check USDA eligibility

A Smarter Strategy for First-Time Buyers

One strategy that’s becoming more common in Harris County:

Start with what you qualify for—then upgrade later.

For example:

- Use FHA or Non-QM to purchase now

- Build equity and improve your financial profile

- Refinance into a conventional loan later

This approach helps buyers enter the market sooner instead of waiting and getting priced out.

Final Thoughts

Finding the right first time home buyer loans in Harris County TX isn’t about chasing the lowest rate—it’s about choosing the loan that actually works for your real-life situation.

The Harris County market moves fast. The buyers who succeed are the ones who understand their options and act strategically.

And in many cases, the “best” loan isn’t the cheapest—it’s the one that gets you into your home at the right time.